CT600L is the supplementary page companies use with their Company Tax Return when claiming R&D Expenditure Credit, the merged R&D expenditure credit scheme, or an SME/ERIS payable tax credit. It does not prove that a project qualifies for R&D tax relief. Its role is to show HMRC how the credit has been calculated, set against Corporation Tax, restricted by notional tax or PAYE/NIC rules, surrendered, carried forward, offset against other liabilities, or paid to the company.

For finance teams, CT600L is where an R&D tax claim becomes a Corporation Tax filing issue. A technically sound claim can still be delayed or rejected if the supporting forms, figures and CT600 boxes do not align.

Area |

Detail |

| Form | CT600L: Company Tax Return supplementary page for research and development |

| Used for | RDEC, merged scheme expenditure credit, SME payable tax credit and ERIS payable tax credit claims |

| Filed with | CT600 Company Tax Return, usually through Corporation Tax software |

| Current HMRC form | CT600L (2026) Version 3 |

| Accounting period limit | The CT600L period cannot exceed 12 months |

| Separate requirement | The Additional Information Form must be submitted before, or on the same day as, the CT600 |

| Claim notification | Some first-time or infrequent claimants must notify HMRC before claiming |

| Main commercial risk | Incorrect sequencing, weak supporting evidence, PAYE cap errors, inconsistent CT600 figures or group surrender mistakes |

You normally need CT600L where the R&D claim produces an expenditure credit or a payable tax credit. This includes:

You do not use CT600L as the technical report. It is a tax return supplementary page. The underlying claim still needs eligible R&D projects, qualifying cost analysis, competent professional input and a complete Additional Information Form.

Use this checklist before CT600L is submitted:

Done |

Pre-filing check |

| ☐ | Has the company confirmed which R&D relief route applies for the accounting period? |

| ☐ | Has the Additional Information Form been completed and sequenced before the CT600? |

| ☐ | Is a claim notification form required? |

| ☐ | Do the qualifying expenditure figures match the claim methodology and computations? |

| ☐ | Do the CT600L figures reconcile to the CT600 and tax computation? |

| ☐ | Has the PAYE/NIC cap been modelled correctly? |

| ☐ | Have connected company PAYE/NIC figures and employer references been checked? |

| ☐ | Are group surrenders, carried-forward amounts and offsets clearly documented? |

| ☐ | Are bank details included where HMRC needs to make a payment? |

| ☐ | Is the technical evidence strong enough to support the claim if HMRC opens a compliance check? |

A robust R&D claim should usually follow this order:

Boxes L1 to L4 identify the company, tax reference and accounting period covered by the supplementary page. The period cannot exceed 12 months, so long periods of account may need more than one return and more than one set of R&D filing data.

Boxes L5 to L9 deal with Step 2 restrictions brought forward from previous accounting periods and RDEC surrendered from group companies. This section matters where the company has older restricted RDEC amounts or is using credit surrendered by another group company.

Boxes L10 to L45 calculate the amount of RDEC or merged scheme expenditure credit available and the amount used to discharge the current period Corporation Tax liability. This is a key cash flow point. The credit may reduce Corporation Tax before any payable balance is considered.

Boxes L50 to L65 apply the notional tax mechanism. The purpose is to reflect that the expenditure credit is taxable and to limit the payable amount so that loss-making and profit-making companies receive an equivalent post-tax benefit.

Boxes L70 to L80 apply the PAYE/NIC cap for RDEC or merged scheme credits where relevant. This section can be problematic where there are connected companies, externally provided workers, subcontracted work, overseas costs, or short accounting periods.

Boxes L85 to L125 show what happens to any remaining credit. It may be offset against other Corporation Tax liabilities, surrendered to a group member, set against other company liabilities, restricted by going concern or other payment rules, or paid to the company.

Boxes L129 to L165 record credits carried forward to later accounting periods or surrendered within a group. These boxes should be consistent with group computations and any recipient company treatment.

Boxes L166 to L190 cover SME payable tax credit and ERIS-related figures. For accounting periods beginning on or after 1 April 2024, this section is relevant where the company qualifies for enhanced R&D intensive support.

Boxes L194 to L210 summarise R&D amounts used to discharge liabilities in the Company Tax Return. These figures feed into the main CT600, so mismatches between the CT600, CT600L and computations can create filing friction or HMRC questions.

The old RDEC and SME schemes have been replaced by two routes for accounting periods beginning on or after 1 April 2024:

Route |

Broad use |

CT600L relevance |

| Merged R&D expenditure credit scheme | Eligible trading companies claiming a taxable expenditure credit | CT600L is used to calculate and allocate the expenditure credit |

| Enhanced R&D intensive support | Loss-making R&D intensive SMEs meeting the intensity condition | CT600L is used where a payable ERIS credit is claimed |

The merged scheme uses a 20% expenditure credit before tax and restrictions. ERIS allows qualifying loss-making R&D intensive SMEs to claim an additional 86% deduction and a payable credit worth 14.5% of the surrenderable loss, subject to the relevant conditions and caps.

For CFOs, the practical issue is scheme selection. A company may be eligible for ERIS but choose the merged scheme for the same expenditure. It cannot claim both schemes for the same costs. The decision should be modelled before the CT600L is completed.

CT600L affects more than tax compliance. It can affect cash timing, Corporation Tax payments, group cash allocation and the recoverability of the expected credit.

The main commercial risks are:

FI Group by EPSA supports companies with R&D tax relief claims from eligibility assessment through to calculation, documentation and filing support. For CT600L, that means helping finance and tax teams connect the technical claim, cost base, Additional Information Form, computations and CT600L entries into one consistent claim file.

Support can include:

A CT600L review is most useful before the Company Tax Return is filed. At that point, errors in sequencing, scheme selection, PAYE cap treatment and CT600 reconciliation can still be corrected.

What is CT600L?

CT600L is the supplementary page used with a Company Tax Return to report certain R&D tax relief claims. It shows how the R&D expenditure credit or payable tax credit is calculated, restricted, offset, surrendered, carried forward or paid.

Is CT600L required for every R&D tax relief claim?

No. It is generally required where the company is claiming RDEC, the merged scheme expenditure credit, SME payable tax credit, ERIS payable credit, or certain SME RDEC amounts. A claim that only creates an SME additional deduction and no payable credit may not need CT600L.

Is CT600L the same as the Additional Information Form?

No. The Additional Information Form provides project, cost and claim information to HMRC before the claim is made. CT600L is the Corporation Tax supplementary page that records the tax calculation and credit treatment.

Do merged scheme claims use CT600L?

Yes. For accounting periods beginning on or after 1 April 2024, merged scheme expenditure credit claims are reported through the Company Tax Return process, with CT600L used to show the credit calculation and how the credit is applied.

How does CT600L apply to ERIS?

For enhanced R&D intensive support, CT600L is relevant where a loss-making R&D intensive SME is claiming a payable tax credit. The SME/ERIS section records qualifying expenditure, PAYE/NIC cap information and the payable credit position.

What happens if the Additional Information Form is submitted after the CT600?

HMRC can reject the R&D claim. If both forms are submitted on the same day, the Additional Information Form should be submitted first, followed by the CT600.

Can CT600L cover more than 12 months?

No. The CT600L period cannot exceed 12 months. A long period of account may need more than one Corporation Tax accounting period, with claim information split accordingly.

What is the PAYE/NIC cap on CT600L?

The PAYE/NIC cap can restrict the payable element of an R&D credit. For accounting periods beginning on or after 1 April 2024, the cap is generally based on £20,000 plus 300% of relevant PAYE and National Insurance contributions, subject to the detailed rules and exemptions.

Can RDEC be surrendered to a group company?

Yes, where the rules allow it. CT600L includes boxes for RDEC surrendered to a group member, and the computations should include details of the other group company and amount surrendered.

Which CT600 boxes does CT600L feed into?

Important CT600L outputs include payable RDEC, SME/ERIS balance payable tax credit and total R&D set-off against liabilities. These figures feed into the main CT600 and should reconcile with the tax computation.

What evidence should support CT600L?

The company should retain project evidence, competent professional input, cost analysis, apportionment methodology, PAYE/NIC cap calculations, scheme selection rationale, Additional Information Form records and CT600 reconciliation schedules.

R&D Capital Allowances, formally known as Research and Development Allowances or RDAs, allow qualifying businesses to claim a 100% capital allowance on eligible capital expenditure used for R&D. They can apply to R&D facilities, laboratories, test rigs, pilot lines, specialist equipment, IT infrastructure and other assets used to carry out or support qualifying R&D. HMRC’s Capital Allowances Manual states that RDA gives relief for capital expenditure on research and development related to the claimant’s trade, and that the rate is 100%.

Question |

Answer |

| What are R&D Capital Allowances? | A 100% capital allowance for qualifying capital expenditure on R&D, also known as Research and Development Allowances or RDAs. |

| Who can claim? | HMRC says RDAs are available to traders where the R&D is related to the trade carried on. |

| What can qualify? | Capital expenditure on R&D directly undertaken by the trader or on the trader’s behalf, subject to conditions. |

| What cannot qualify? | HMRC states that no allowances are due for expenditure on acquiring land or rights in or over land. |

| Is the rate really 100%? | Yes. HMRC states that the RDA rate is 100% of qualifying expenditure, subject to disposal-value rules. |

| Can you claim less than 100%? | Yes, but HMRC says if a reduced amount is claimed, the balance cannot be claimed later. |

| Is this the same as R&D tax relief? | No. R&D tax relief normally focuses on qualifying revenue expenditure. RDAs are for capital expenditure on R&D. |

| How is it claimed? | Capital allowances are claimed through the relevant tax return. Limited companies claim through the Company Tax Return with a separate capital allowances calculation. |

| Why does this matter now? | Capital allowance rules have changed, including full expensing from 1 April 2023, a 40% first-year allowance for qualifying assets bought from 1 January 2026 and a main pool writing down allowance rate of 14% from April 2026. |

Many innovative companies invest heavily in physical and digital infrastructure before they fully understand the tax treatment. That can include laboratories, clean rooms, production trials, pilot plants, test equipment, engineering facilities, specialist software infrastructure, manufacturing lines, robotics, environmental testing areas or technical fit-outs.

These costs often sit outside a standard R&D tax credit claim because they are capital in nature. HMRC’s R&D tax relief guidance says capital expenditure is excluded from qualifying R&D expenditure, although it may qualify for R&D allowances. HMRC also notes that accounts treatment is not conclusive when deciding whether expenditure is revenue or capital for tax purposes.

For FI Group clients, this is where value is often missed. A company may claim R&D tax relief on staff, consumables, subcontractors or software, but fail to review the capital investment that made the R&D possible.

Research and Development Allowances are a type of capital allowance. They are designed to give tax relief for capital expenditure on R&D that is related to a trade carried on by the claimant.

HMRC says qualifying RDA expenditure is capital expenditure incurred on R&D directly undertaken by the trader, or on the trader’s behalf, provided the R&D is related to a trade the trader carries on, or a trade the trader sets up and commences that is connected with the R&D.

In practical terms, RDAs may be relevant where a company spends money on assets or facilities used to carry out R&D, rather than only on day-to-day project costs.

Examples can include:

Asset or spend type |

Why it may be relevant |

| Laboratory fit-out | Can support qualifying scientific or technological R&D activity. |

| Pilot production line | May be used to test, validate or improve a new process before commercial scale-up. |

| Test rigs and testing equipment | Often directly connected to resolving technological uncertainty. |

| Specialist plant and machinery | May be required to conduct experiments, trials or development work. |

| Technical IT infrastructure | Can support R&D activity where it is capital in nature and directly linked to the R&D. |

| R&D facility refurbishment | May qualify where the expenditure is on facilities used for R&D and the land element is excluded. |

| Clean rooms, controlled environments or environmental chambers | Can be central to life sciences, advanced manufacturing, electronics, materials or energy R&D. |

R&D tax relief and R&D Capital Allowances are related, but they do different jobs.

Area |

R&D tax relief |

R&D Capital Allowances |

| Main purpose | Relief for qualifying R&D expenditure under the R&D tax regime. | Capital allowance relief for qualifying capital expenditure on R&D. |

| Typical costs | Staff, EPWs, subcontractors, consumables, software, cloud and data where eligible. | R&D facilities, equipment, laboratories, pilot plant and other capital assets. |

| Tax nature | Usually revenue expenditure, although capitalised accounting treatment needs tax analysis. | Capital expenditure. |

| Claim route | Company Tax Return, with claim notification and AIF requirements where relevant. | Capital allowances calculation in the tax return. |

| Key risk | Weak technical evidence, cost eligibility, AIF quality and scheme treatment. | Misclassifying capital vs revenue, missing RDA, using the wrong allowance or failing to evidence R&D use. |

| FI Group role | Technical and financial R&D claim preparation, AIF support and enquiry readiness. | Identifying R&D-related capital expenditure, mapping costs and supporting robust capital allowance treatment. |

FI Group’s R&D tax page already explains that R&D tax claims involve technical uncertainty, evidence, cost mapping and HMRC requirements such as claim notification and the Additional Information Form. The R&D Capital Allowances page should connect that same evidence-led approach to capital investment in R&D assets.

Not every R&D asset automatically sits under RDA. The best treatment depends on what was bought, who bought it, when it was bought, whether it is new or used, whether it is plant and machinery, whether it forms part of a building and whether it is used for qualifying R&D.

Allowance |

Current treatment |

Where it may fit |

| Research and Development Allowances | 100% allowance for qualifying capital expenditure on R&D. | R&D facilities, laboratories, pilot plants, test assets and capital assets used for R&D. |

| Annual Investment Allowance | AIA is £1 million and can apply to most plant and machinery, subject to exclusions. | General plant and machinery, including many assets used in R&D, where AIA is available and sufficient. |

| Full expensing | Companies can deduct 100% of the cost of qualifying new and unused plant and machinery bought from 1 April 2023. | New main-rate plant and machinery where the company meets the conditions. |

| 50% first-year allowance | Companies can deduct 50% of qualifying expenditure on certain special rate assets bought from 1 April 2023. | Special-rate plant and machinery such as some integral features. |

| 40% first-year allowance | Qualifying plant or machinery bought on or after 1 January 2026 can receive a 40% first-year allowance, with writing down allowances on the remaining 60%. | Main-rate plant and machinery that meets the conditions. |

| Writing down allowances | Main pool rate is 14% from April 2026, previously 18%; special rate pool is 6%. | Assets not fully relieved through RDA, AIA or first-year allowances. |

| Structures and Buildings Allowance | 3% straight-line relief for qualifying non-residential structures and buildings. | Building expenditure that does not qualify for RDA or plant and machinery allowances. |

Standard capital allowances can be useful, but they do not always give the best treatment for R&D-related capital investment.

For example, a non-residential building may otherwise fall into Structures and Buildings Allowance at 3% a year, while certain integral features may sit in the special rate pool at 6% a year. Where the expenditure qualifies as RDA, HMRC’s manual states the rate is 100%, which can materially accelerate relief compared with slower writing down allowances or SBA.

The key issue is classification. A finance team should not assume that all R&D-related assets are treated in the same way. The right analysis may split one project across RDAs, AIA, full expensing, special rate pool, main pool and SBA.

A claim should start with the R&D purpose of the asset or facility. The expenditure must be capital in nature and connected to R&D related to the trade.

Potentially relevant expenditure can include:

R&D facilities

This can include laboratories, testing areas, pilot production areas, specialist build-outs and controlled environments where the facility is used to carry out qualifying R&D.

Specialist plant and machinery

Equipment used to test, validate, measure, process, manufacture, simulate or improve new products, materials, systems or processes may be relevant where it supports qualifying R&D activity.

Pilot plant and test rigs

Pilot plants and test rigs can be central to resolving technological uncertainty. The capital treatment needs to be mapped carefully against R&D purpose, commercial use and future use.

R&D-related IT infrastructure

Servers, specialist computing infrastructure, internal platforms or technical systems may be relevant where they are capital in nature and directly support R&D.

Fit-out and refurbishment

Where a company refurbishes or fits out a space for R&D activity, the spend should be analysed. Some elements may be RDA, some may be plant and machinery, some may be integral features, some may be SBA and land must be excluded where relevant.

HMRC states that no allowances are due for expenditure on acquiring land or rights in or over land. Where expenditure is incurred on a building, structure or fixed plant and machinery, a just apportionment may be required to exclude the land element.

A UK engineering company invests £3 million in a new technical development facility.

| Cost category | Spend | Possible treatment |

| R&D test rigs and specialist equipment | £900,000 | Potential RDA or plant and machinery treatment, depending on facts. |

| Pilot line and technical installation | £800,000 | Potential RDA where directly used for R&D, or plant and machinery allowances. |

| Laboratory and controlled test environment fit-out | £700,000 | Potential RDA, with detailed cost mapping required. |

| Office refurbishment and general admin areas | £350,000 | Less likely to qualify as RDA; may fall under other capital allowance categories. |

| Land element | £250,000 | Excluded from RDA. |

A surface-level review might treat this as a normal building and equipment project. A stronger review separates:

This is where specialist review matters. The tax result depends on the evidence, the use of the assets, the cost breakdown and how the R&D activity is documented.

R&D Capital Allowances often overlap with commercial property. A company may buy, lease, build or refurbish a site that includes fixtures, plant, machinery, integral features and R&D-specific facilities.

GOV.UK states that plant and machinery can include integral features and fixtures, including lifts, heating systems, air-conditioning, hot and cold water systems, electrical systems including lighting, external solar shading, fitted kitchens, bathroom suites, fire alarms and CCTV systems. It also states that when buying a building from a previous business owner, the buyer can usually only claim for integral features and fixtures that the seller claimed for, and the fixture value must be agreed with the seller.

For second-hand fixtures, HMRC’s Capital Allowances Manual says the availability of capital allowances to a purchaser is generally conditional on the seller pooling relevant expenditure before transfer and the seller and purchaser formally agreeing a value within two years of transfer, or commencing formal proceedings within that time.

For innovation businesses, this means property transactions should not be handled as a purely legal or real estate issue. Capital allowances need to be reviewed before completion where possible, especially if the property includes labs, specialist facilities or embedded technical systems.

Mistake |

Why it matters |

How to avoid it |

| Treating all R&D spend as R&D tax relief | Capital expenditure is excluded from qualifying R&D tax relief, although it may qualify for RDAs. | Separate revenue and capital expenditure before preparing the R&D claim. |

| Missing RDAs on R&D facilities | R&D buildings, facilities and fit-outs may be reviewed only as property spend. | Review the R&D purpose of each asset and area. |

| Assuming AIA or full expensing is always best | RDA may accelerate relief where the expenditure qualifies. | Compare RDA, AIA, full expensing, WDA and SBA before filing. |

| Not excluding land | Land does not qualify for RDA. | Use a just and reasonable apportionment where needed. |

| Claiming less than 100% RDA without planning | HMRC says if a reduced RDA amount is claimed, the balance cannot be claimed later. | Model profit, losses, group relief and future tax position before deciding. |

| No asset-use evidence | The R&D purpose of the asset must be supportable. | Keep project records, technical sign-off and asset-use documentation. |

| Poor fixed asset register detail | Broad categories hide qualifying expenditure. | Map invoices and assets into tax-relevant categories. |

| Missing second-hand fixture rules | Property acquisitions can lose value if pooling and value-fixing are not handled. | Review capital allowances before completion and align with legal documents. |

| Treating commercial scale-up as automatically R&D | Pilot and test phases may qualify, but normal commercial production may not. | Document the point at which R&D ends and commercial use begins. |

| Ignoring post-project use | Asset use can change after R&D. | Track R&D use, commercial use and disposal events. |

FI Group helps companies identify, evidence and claim the right tax relief for innovation-related capital investment. We work with finance, tax, technical, property and operational teams to connect the asset spend to the underlying R&D activity.

FI Group’s R&D claim support already covers technical evidence, cost mapping, Additional Information Form requirements and enquiry defence. The R&D Capital Allowances service should be positioned as a complementary review for capital investment in innovation assets.

Speak to FI Group before filing if your business has:

The Additional Information Form, often called the AIF, is a mandatory HMRC form used to support R&D tax relief and R&D expenditure credit claims. It must be submitted before or on the same day as the Company Tax Return, CT600. If the AIF and CT600 are submitted on the same day, the AIF must be submitted first. If the CT600 is submitted first, HMRC can reject the R&D claim.

FI Group helps companies prepare accurate, evidence-led AIF submissions that align with the R&D claim, technical project descriptions, qualifying costs, tax computations and CT600 filing process.

Question |

Answer |

What is the Additional Information Form? |

The AIF is an HMRC online form that gives supporting details for an R&D tax relief or R&D expenditure credit claim. |

Is the AIF mandatory? |

Yes, for companies making new R&D tax relief, expenditure credit or combined claims. |

When must the AIF be submitted? |

Before or on the same day as the CT600. If submitted on the same day, the AIF must go first. |

What happens if the CT600 is submitted first? |

HMRC can reject the R&D claim and remove it from the Company Tax Return. |

Is the AIF the same as claim notification? |

No. The AIF supports the claim. Claim notification is a separate step that applies to some first-time or returning claimants. |

Who can submit the AIF? |

A company representative or an agent acting on behalf of the company. |

Do I need one AIF for each accounting period? |

Yes. If your period of account is longer than 12 months and creates more than one Corporation Tax accounting period, you may need more than one AIF. |

What does the AIF include? |

Company details, accounting period dates, senior R&D contact details, agent details, qualifying expenditure, R&D intensity details where relevant and project descriptions. |

Can I access the AIF after submitting it? |

HMRC says you should save a copy before submission because the form cannot be accessed once submitted. |

Why does the AIF matter? |

It is one of the first documents HMRC sees when assessing whether an R&D claim is credible, complete and technically defensible. |

The AIF is not a minor administrative step. It is a core part of the R&D tax relief claim process.

For HMRC, the form gives structured information about:

Before submitting the Additional Information Form, use this checklist to confirm the claim is ready.

|

Complete |

AIF preparation check |

|

☐ |

The company has confirmed which R&D scheme applies. |

|

☐ |

Claim notification has been checked separately. |

|

☐ |

The AIF accounting period matches the CT600. |

|

☐ |

Longer periods of account have been split correctly. |

|

☐ |

UTR, PAYE, VAT and SIC details are available. |

|

☐ |

Northern Ireland company details have been checked where relevant. |

|

☐ |

A senior internal R&D contact has been identified. |

|

☐ |

All agents involved in the claim have been listed. |

|

☐ |

R&D intensity details have been prepared where relevant. |

|

☐ |

Connected company costs have been reviewed where relevant. |

|

☐ |

Qualifying expenditure has been reconciled by category. |

|

☐ |

Project selection rules have been applied. |

|

☐ |

Each project description covers field, baseline, advance, uncertainty and method. |

|

☐ |

Costs can be linked to the selected projects. |

|

☐ |

|

|

☐ |

A copy of the AIF will be saved before submission. |

|

☐ |

The HMRC confirmation reference will be retained. |

|

☐ |

The R&D technical report and evidence pack are ready. |

For claimants, the AIF creates a higher standard of evidence. A weak AIF can make a genuine claim look unclear. A strong AIF connects the technical work, financial data and tax return into one consistent position.

This is especially important for businesses in:

In these sectors, R&D activity is often complex. The challenge is not only proving that innovation happened. It is proving that the claim meets HMRC’s definition of R&D for tax purposes and that the costs have been mapped correctly.

The AIF is often confused with claim notification. They are not the same.

Requirement |

What it does |

Who it affects |

Timing |

|

Additional Information Form |

Gives HMRC detailed technical and financial information before the R&D claim is made. |

Companies making new R&D tax relief or expenditure credit claims. |

Before or on the same day as the CT600, with the AIF submitted first if both are sent on the same day. |

|

Tells HMRC in advance that a company intends to claim R&D tax relief. |

Some first-time claimants and some returning claimants whose last claim was made more than 3 years before the last date of the claim notification period. |

Usually within the claim notification period, which ends 6 months after the period of account. |

|

|

The tax return where the R&D tax relief or expenditure credit claim is made. |

Companies claiming Corporation Tax R&D relief. |

Usually filed within 12 months of the end of the accounting period. |

|

|

Supplementary R&D page used in relevant R&D expenditure credit, merged scheme, ERIS or payable credit situations. |

Companies claiming expenditure credit or payable R&D credits where required. |

Filed with the Company Tax Return. |

|

|

Supporting evidence explaining eligibility, project work, uncertainties and methodology. |

Not always submitted as a mandatory form, but often important for enquiry readiness. |

Prepared before the AIF and CT600 so the claim is consistent. |

The AIF should be treated as part of a wider R&D claim pack, not as a standalone online form. The strongest claims align the AIF with the CT600, CT600L, tax computations, project evidence, competent professional input and cost methodology.

A company making a new R&D tax relief, R&D expenditure credit or combined claim must submit an Additional Information Form to support the claim.

This includes claims under:

The AIF can be completed by the:

If an agent submits the form, they need the correct HMRC agent services access and the company’s permission.

The AIF is not only for first-time claimants. The “first-time claimant” and “returning claimant after 3 years” rules relate to claim notification, not the AIF. Many companies need to consider both steps.

The AIF must be submitted before or on the same day as the CT600.

The safest sequence is:

If the AIF and CT600 are submitted on the same day, the AIF should be submitted first. Filing the CT600 first can cause the R&D claim to be rejected.

The AIF asks for structured information about the company, the accounting period, the people involved in the claim, the costs and the R&D projects.

You should prepare:

Information |

Why it matters |

|

Unique Taxpayer Reference, UTR |

Must match the Company Tax Return. |

|

Employer PAYE reference number |

Supports staff cost and PAYE-related checks. |

|

VAT registration number |

Identifies the company where applicable. |

|

SIC code or business type |

Helps HMRC understand the company’s activities. |

|

Company Registration Number, where relevant |

Needed for Northern Ireland companies. |

|

Registered business address, where relevant |

Needed for Northern Ireland companies. |

The AIF asks for:

The senior internal contact should understand the R&D claim and be able to explain the projects. This should not be someone who only has a surface-level view of the business.

Agent details matter because HMRC wants visibility over everyone involved in preparing, advising on or submitting the claim.

The AIF accounting period dates must match the Company Tax Return.

This is a basic point, but it is a common source of risk. If the accounting period on the AIF does not match the CT600, the form can be rejected and the R&D claim can be removed.

Where a period of account is longer than 12 months, there may be more than one Corporation Tax accounting period. In that case, the company may need to submit more than one AIF.

The AIF can require additional information where the company is claiming Enhanced R&D Intensive Support or where R&D intensity is relevant.

This can include:

This matters because the R&D intensity calculation is not always limited to the claimant company in isolation. Group structure, connected companies and overseas connected entities may affect the position.

Do not leave R&D intensity analysis until the AIF is being submitted. It should be reviewed early, especially for groups, scale-ups, international structures and companies with uneven R&D spend across accounting periods.

The number of project descriptions required depends on how many R&D projects are included in the claim.

Number of projects claimed |

What the AIF requires |

|

1 to 3 projects |

Describe each project. |

|

4 to 10 projects |

Describe at least 3 projects, and those projects must account for at least half of the qualifying expenditure. |

|

More than 10 projects |

Describe at least 3 projects covering at least half of the qualifying expenditure. If more than 10 projects would be needed to reach half of the expenditure, select the 10 projects with the highest qualifying expenditure. |

If the company is claiming both SME tax relief and expenditure credit in the same accounting period, project details may need to be provided separately for each claim.

This makes project selection important. The AIF should not be completed by picking easy-to-describe projects if they do not represent the main qualifying expenditure. HMRC expects the selected projects to give a meaningful view of the claim.

The project description is the most important part of the AIF. It should be clear enough for HMRC to understand why the work qualifies for R&D tax purposes.

Each project description should cover the following areas.

Describe the field of science or technology the project relates to.

This should be specific. Avoid broad descriptions such as “software”, “engineering” or “manufacturing” if the real field is more precise.

Better examples include:

Explain what was already known or possible at the start of the project.

This is where many AIF submissions are weak. The baseline should not just describe the company’s starting point. It should explain the wider scientific or technological capability available in the field.

A good baseline answers:

Explain the advance the company aimed to achieve.

The advance must be in science or technology, not simply in commercial performance. A new product, faster internal process or more profitable service is not enough unless it depends on resolving scientific or technological uncertainty.

A good advance explains:

Set out what was uncertain and why it could not be readily resolved by a competent professional.

This should not be a generic project risk. Budget constraints, lack of staff, user adoption, supplier delays or commercial uncertainty do not normally demonstrate R&D for tax purposes.

A strong uncertainty explains:

Explain the R&D activities carried out.

This can include:

The description should show a logical link between the uncertainty and the work done to resolve it.

The AIF should connect the project narrative to the costs being claimed.

This means the technical description should not sit separately from the financial analysis. The project selected, the activities described and the qualifying expenditure should all reconcile.

Weak description |

Stronger approach |

|

“We developed a new software platform for customers.” |

Explain the technological field, the existing capability, the specific technical limitation, the uncertainty faced and the development work undertaken to resolve it. |

|

“The project was innovative because no competitor offered this feature.” |

Explain the scientific or technological advance, not only the market novelty. |

|

“The team had technical challenges during development.” |

Identify the uncertainties that a competent professional could not readily resolve. |

|

“We improved our manufacturing process.” |

Explain the process baseline, the target advance, the variables tested, the technical constraints and the experimental work. |

|

“We claimed 50% of staff time.” |

Explain how time was allocated to qualifying R&D activities and how the methodology is evidenced. |

Mistake |

Why it is a problem |

How to avoid it |

|

Confusing AIF with claim notification |

They are separate requirements. One does not replace the other. |

Check both requirements before preparing the claim. |

|

Submitting the CT600 before the AIF |

HMRC can reject the R&D claim. |

Submit the AIF first and keep the reference. |

|

Incorrect accounting period dates |

Date mismatches can cause rejection. |

Match the AIF exactly to the CT600. |

|

Generic project descriptions |

HMRC may not understand why the work qualifies. |

Use field, baseline, advance, uncertainty and method. |

|

Describing commercial innovation only |

R&D tax relief is focused on science or technology. |

Separate commercial benefits from technological advances. |

|

Missing all agents involved |

HMRC asks for details of all agents involved in the claim. |

Record every adviser who contributed to the claim, cost analysis, technical assessment, forms or CT600. |

|

No senior internal contact |

HMRC expects a senior internal R&D contact. |

Identify someone who understands the R&D and can support the claim. |

|

Costs do not reconcile |

Inconsistent AIF, computation and CT600 figures create risk. |

Reconcile costs by project and category before submission. |

|

Wrong project sample |

The selected projects may not represent enough qualifying expenditure. |

Apply HMRC’s project selection rules before drafting. |

|

Not saving the AIF |

HMRC says the form cannot be accessed after submission. |

Save a copy before submitting and keep the confirmation reference. |

|

Leaving the AIF until filing day |

Rushed forms create errors and weak narratives. |

Prepare the AIF alongside the R&D technical report and cost review. |

|

Ignoring Northern Ireland and ERIS details |

Additional declarations may be needed. |

Check registered office, sector, de minimis aid and ERIS position early. |

If the AIF is not submitted correctly, the R&D claim may not be accepted.

The most serious risk is sequencing. If the Company Tax Return is submitted before the AIF, HMRC can reject the claim and remove it from the CT600. If the company is close to the amendment deadline, there may not be enough time to make a valid claim for that accounting period.

Other risks include:

How FI Group helps with the Additional Information Form

FI Group helps companies prepare AIF-ready R&D tax relief claims that are technically robust, financially reconciled and ready for submission before the CT600.

Our support includes:

The AIF is now a central part of the R&D tax relief process. These FAQs answer the most common questions companies ask before preparing, submitting or reviewing their Additional Information Form.

What is the Additional Information Form?

The Additional Information Form is an HMRC online form that provides supporting information for an R&D tax relief or R&D expenditure credit claim. It includes company details, contact details, accounting period details, qualifying expenditure and R&D project descriptions.

Is the Additional Information Form mandatory?

Yes. Companies making new R&D tax relief, expenditure credit or combined claims must submit an AIF to support the claim.

When do I need to submit the AIF?

The AIF must be submitted before or on the same day as the CT600 Company Tax Return. If both are submitted on the same day, the AIF should be submitted first.

What happens if I submit the CT600 before the AIF?

The R&D claim can be rejected. HMRC can remove the R&D claim from the Company Tax Return, which may cause serious issues if the amendment deadline is close.

Is the AIF the same as the claim notification form?

No. The AIF supports the R&D claim with detailed technical and financial information. Claim notification is a separate form that tells HMRC in advance that some companies intend to claim.

Who needs to submit a claim notification form?

Claim notification applies to some first-time claimants and some returning claimants whose last claim was made more than 3 years before the last date of the claim notification period. It applies to accounting periods beginning on or after 1 April 2023.

Can an agent submit the AIF?

Yes. An agent can submit the AIF on behalf of the company if they have the correct agent services access and the company’s permission.

What information do I need before starting the AIF?

You need company details, accounting period dates, senior internal R&D contact details, agent details, qualifying expenditure, project details and R&D intensity information where relevant.

How many projects do I need to describe?

If you are claiming for 1 to 3 projects, describe all projects. If you are claiming for 4 to 10 projects, describe at least 3 projects covering at least half of the qualifying expenditure. If you are claiming for more than 10 projects, describe at least 3 projects covering at least half of the expenditure, with a maximum of the 10 highest expenditure projects where needed.

What should each project description include?

Each project description should explain the main field of science or technology, the baseline level of knowledge, the advance sought, the scientific or technological uncertainties and the work undertaken to overcome those uncertainties.

Do I still need an R&D technical report?

In most cases, yes. The AIF is a structured HMRC form, but a technical report can provide fuller evidence of eligibility, methodology, competent professional input and cost mapping.

Can I access the AIF after submitting it?

HMRC advises claimants to save a copy before submitting because the form cannot be accessed after submission.

How can FI Group help with the AIF?

FI Group can review your claim position, prepare project descriptions, map qualifying costs, check claim notification requirements, support CT600 alignment and build an enquiry-ready evidence pack before submission.

In the dynamic landscape of business innovation, understanding government incentives is pivotal. One such incentive in the UK that plays a crucial role in fostering research and development is the Research and Development Expenditure Credit (RDEC).

In this detailed exploration, we unravel the intricacies of RDEC, providing a comprehensive understanding of its significance, eligibility criteria, and how it contributes to the growth of businesses.

The Research and Development Expenditure Credit, commonly known as RDEC, stands as a pivotal component of the UK government’s initiative to encourage and support innovation among businesses, particularly larger enterprises.

Introduced in 2013, RDEC plays a vital role in incentivising companies to invest in research and development activities, thereby contributing to technological advancements and economic growth.

Understanding these rates becomes extremely important as they play a significant role in driving innovation by offering financial incentives to businesses

The RDEC scheme distinguishes itself by allowing companies to claim their R&D credits “above-the-line” as taxable income. This is a notable departure from the traditional below-the-line benefit seen in the SME R&D scheme. The shift aims to provide a more direct and visible financial incentive, positioning R&D credits as a part of taxable income.

This transformation is not merely procedural but a strategic decision that increases visibility and provides a real boost to a company’s financial profile. By spotlighting R&D credits as integral components of taxable income, it influences investor perceptions and strengthens the UK’s position as an R&D hub.

To make an RDEC claim, companies must meet specific eligibility criteria. Larger businesses, recipients of Notified State Aid, SMEs with partner and linked enterprises, and subcontractors fall under the purview of the RDEC scheme. This ensures that a diverse range of entities engaged in research and development activities can benefit from the incentives provided by RDEC.

Navigating these criteria is key to optimizing RDEC rates. The evolving corporate tax landscape, with the main corporation tax rate increasing from 19% to 25% in April 2023, necessitates a recalibration of RDEC calculations to maximize benefits effectively.

In 2013, a significant shift occurred in the accounting treatment of RDEC, marking a move to “above-the-line” presentation. This alteration aimed to showcase the R&D credit as income when calculating profit before tax for the departments engaged in R&D. Beyond its intended purpose, this change has broader benefits, enhancing the appeal of businesses to investors and public markets, especially multinational companies deciding on R&D locations.

Understanding the types of costs that qualify for RDEC is paramount. Subcontracted R&D plays a crucial role, and specific criteria for qualifying bodies come into play. Notably, subcontracted R&D is eligible for RDEC, with a focus on individuals, partnerships, or qualifying bodies.

The Research and Development Expenditure Credit (RDEC) stands as a catalyst for businesses aiming to innovate and contribute to technological advancements. With the recent increase in the RDEC rate to 20%, businesses have a prime opportunity to leverage these incentives for growth.

The recent surge in RDEC rates presents a unique opportunity for businesses to enhance their R&D initiatives. The strategic use of consultants, such as FI Group, can ensure a more seamless and rewarding RDEC journey, helping businesses align with these changes and fully capitalize on the increased incentives.

For businesses seeking expert guidance in optimising RDEC claims, FI Group offers in-depth expertise and tailored consultations. We provide a holistic approach, ensuring your business is at the forefront of innovation support while navigating the evolving R&D tax credit landscape effectively.

With a proven track record in assisting companies through the intricate landscape of R&D tax credits, FI Group UK is dedicated to maximising your benefits under the Research and Development Expenditure Credit (RDEC) scheme.

Miss the Claim Notification Form (CNF) deadline and the technical quality of your R&D claim may stop mattering. For first-time and lapsed claimants, the filing position can be simple: notify HMRC in time, or lose the claim for that period. The form is separate from the Additional Information Form and the CT600.

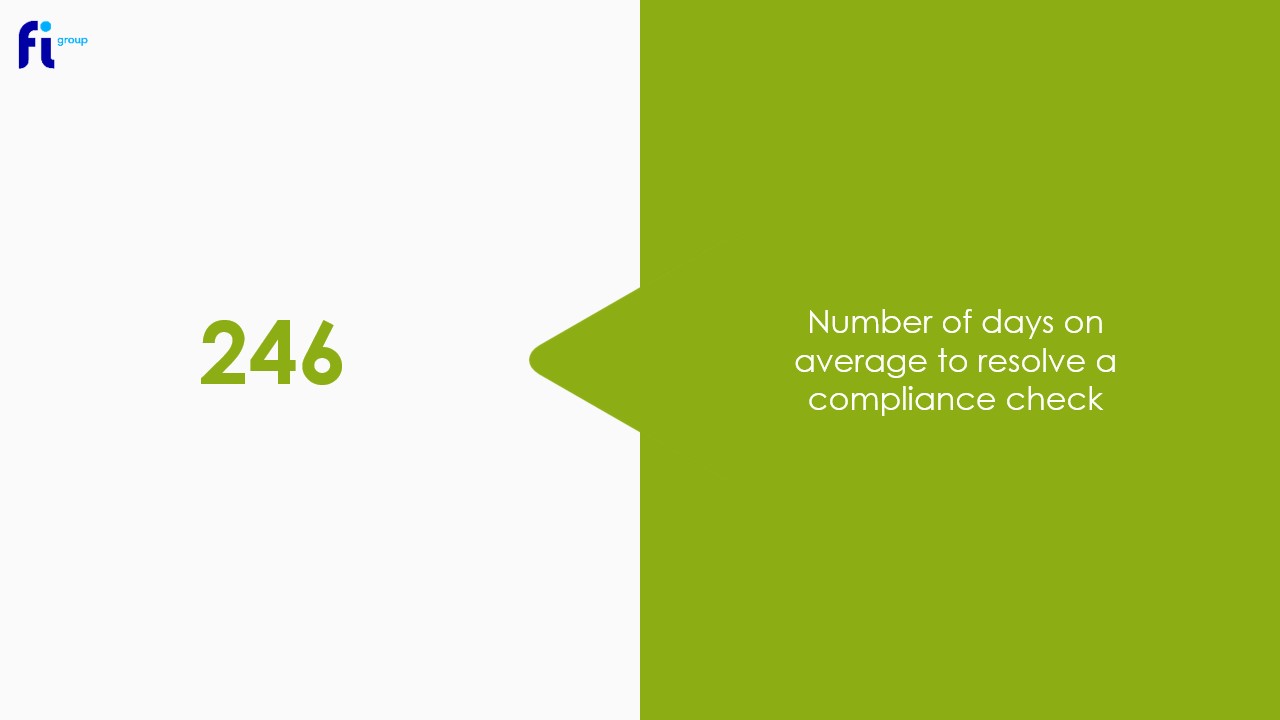

Finance teams also need to look at the timing risk in context. HMRC says it checked 17% of claims in 2023 to 2024, the average compliance check took 246 days, and 77% of settled checks required an adjustment. That is a cash flow issue, a governance issue, and a workload issue.

The Claim Notification Form is HMRC’s advance notice requirement for certain companies intending to claim R&D tax relief. It is not the claim itself, and it does not replace the Additional Information Form or the Company Tax Return.

The rule sits inside the reformed R&D claims process introduced after the Finance (No. 2) Act 2023. HMRC’s internal manual ties the claims process to the Corporation Tax Act 2009, and the 2023 Regulations set out the information that must be included in a claim notification.

You usually need to submit a Claim Notification Form if you are claiming R&D tax relief for the first time, or if your last claim was made more than three years before the last day of the claim notification period.

In practice, that usually catches:

HMRC also lists two published exceptions where a previous claim does not remove the need to notify:

There is one further point that matters. If the actual R&D claim reaches HMRC by the last day of the claim notification period, that can remove the need for a separate form. Many companies miss that detail, then leave the work too late for it to help them.

Scenario |

Claim Notification Form needed? |

| First-ever R&D claim | Yes |

| Recent valid claim inside the three-year lookback, with no exceptions | Usually no |

| Previous R&D claim removed by HMRC from the return | Yes |

| Previous claim for a pre-1 April 2023 period made by amendment received on or after 1 April 2023 | Often yes |

| Long period of account covering more than one accounting period | One notification can cover the period of account, if notification is needed |

The detail still needs to be checked against the company’s own dates and filing history.

The deadline is the end of the “claim notification period”, which runs from the first day of the period of account to six months after the end of that period of account. Miss that deadline and the R&D claim can be invalid.

This is where many finance teams trip up. HMRC does not ask you to look only at the accounting period on the CT600. You also need to understand the period of account used in the financial statements.

For many businesses with a normal 12-month year end, the timing is straightforward. If your period of account ends on 31 March 2025, the last date to notify is 30 September 2025.

For long periods of account exceeding 12 months, the position is more technical. A single period of account can contain two accounting periods for Corporation Tax, but HMRC applies the same claim notification period across those accounting periods. That means one timely notification can cover the accounting periods falling within that same period of account.

| Scenario | Does the company need to notify? | Practical deadline |

| First-ever R&D claim, year end 31 March 2025 | Yes | 30 September 2025 |

| Claimed recently within the relevant three-year window | Usually no | No separate notification needed |

| Last valid claim was too old to fall within the lookback | Yes, unless the actual claim is filed by the last date of the claim notification period | Six months after period of account end |

| 18-month period of account with two CT accounting periods | Often yes for first-time or lapsed claimants, but one notification can cover both periods in that same period of account | Six months after the end of the full period of account |

These examples apply HMRC’s current timing rules and are useful for internal planning, but finance teams should still map the exact dates against the company’s own year-end structure.

A company does not usually need to submit the form if it has made an R&D claim within the three years ending with the last day of the claim notification period, unless one of HMRC’s stated exceptions applies.

There is another important nuance. If a company needs to notify, it can still avoid a separate notification form if the actual R&D claim itself is received by HMRC on or before the last date of the claim notification period. In other words, the claim can sometimes satisfy the timing requirement if it is filed early enough.

That point is valuable for CFOs because it turns the issue into a timetable question, not just a tax technicality. If your finance team will not have the technical narrative, cost schedules, and governance approvals ready early, you should not assume the claim can simply be accelerated to solve the problem.

HMRC’s internal manual, updated in March 2026, records an administrative easement for certain companies affected by incorrect HMRC guidance published between September and October 2024. The easement is narrow and fact-specific, so it should not be treated as a general safety net.

The Claim Notification Form, if required, comes first. The Additional Information Form must then be filed before, or on the same day as, the CT600 claim. Missing either step can invalidate the R&D claim.

For most claimants, the filing sequence should look like this:

This is why finance leaders should treat claim notification as part of claim governance, not as a minor admin step. The technical narrative might be excellent, but the claim can still fail on process.

The biggest mistakes are timing errors, filing sequence errors, and overconfidence in old processes. In the current compliance environment, those mistakes can create cash flow delays, management distraction, and a harder path for future claims.

The most common issues are:

This is the classic deadline error. Teams look at the CT600 period but forget the statutory deadline is tied to the period of account.

The exemption is not a vague “we claimed once before”. It is a specific three-year lookback test, with published exceptions.

HMRC’s guidance is explicit. If the AIF is filed after the return, the R&D claim can be rejected.

The form is only an early notice. The real evidential burden still sits in the AIF, the CT600, and the supporting technical and financial records.

For CFOs, this is where process risk becomes business risk. HMRC’s own 2023 to 2024 figures show both higher compliance coverage and long resolution times, which means poor filing discipline can turn into a serious cash flow issue.

A good process starts early, has named internal ownership, and leaves enough time between each filing step. It does not rely on year-end guesswork.

A practical checklist for finance teams:

The Claim Notification Form is not just a tax form. It is an early control point in the wider governance of your R&D claim. If you miss it, the problem is binary. If you get it right, you still need the AIF, CT600 accuracy, and evidence stack behind the claim.

For finance leaders, the real issue is predictability:

That is why this topic should be owned as part of the annual compliance calendar, not parked until the tax return is nearly ready.

The UK still relies mainly on notification plus post-claim checking, but the policy direction is moving towards more targeted pre-claim assurance. HMRC concluded its consultation on R&D tax relief advance clearances and says it will launch a limited pilot of a new targeted advance assurance service in Spring 2026, while the existing advance assurance offer continues.

That matters for multinational and internationally ambitious groups. HMRC’s consultation notes that many countries already use some form of pre-approval or advance assurance, while the UK is exploring a more targeted model. HMRC also notes that its current advance assurance process has had very low uptake.

For UK groups with overseas operations, the wider lesson is clear: R&D incentives are becoming more process-driven, more evidence-led, and more front-loaded. FI Group by EPSA’s value in that environment is the ability to align HQ strategy with local filing rules, so your UK claim notification, AIF, and wider international governance all work together.

FI Group by EPSA helps CFOs and finance teams turn R&D tax relief from a reactive filing exercise into a controlled process.

We support clients by:

That is where Global Reach. Local Expertise. becomes practical, not just promotional. One group standard, applied properly to the UK rules.

This section answers the questions finance teams most often ask when planning an R&D claim.

Yes. “Advanced Notification Form” or ANF is common market shorthand, but HMRC’s current guidance uses Claim Notification Form.

No. You usually only need it if you are a first-time claimant or your last qualifying claim falls outside the relevant three-year lookback, subject to HMRC’s exceptions.

Yes. HMRC says the form can be submitted by a company representative or an authorised agent.

Not always. HMRC says the actual R&D claim can satisfy the timing requirement if it is received by the last date of the claim notification period.

Yes, where those accounting periods fall within the same period of account, the claim notification period is the same.

No. The Claim Notification Form is an advance notice requirement for certain claimants. The AIF is the detailed information HMRC requires before or alongside the claim itself.

HMRC’s guidance says the R&D claim can be rejected if the AIF is filed after the return.

No. Advance assurance is a separate voluntary HMRC process. The current public guidance says it is aimed at first-time SME claimants below certain size thresholds, and HMRC is also developing a more targeted pilot.

Yes. HMRC’s manuals were updated in March 2026, and HMRC has also confirmed a targeted advance assurance pilot is due to launch in Spring 2026.

Build the claim timetable backwards from the period of account end date, check notification status early, prepare the AIF before the CT600, and do not rely on prior filing habits.

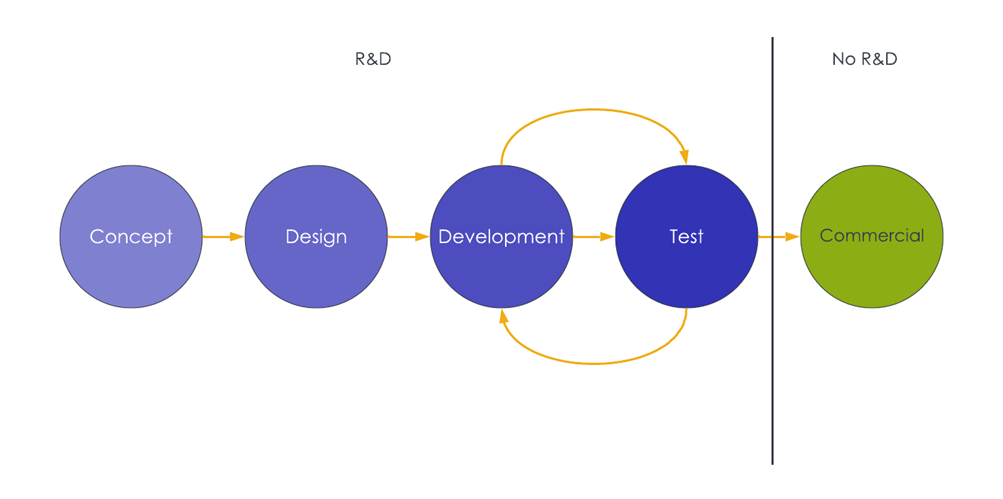

In an R&D claim, the competent professional is the person whose technical judgement helps establish whether the work sought a genuine advance in science or technology, whether scientific or technological uncertainty existed, and where the qualifying R&D began and ended. If that judgement is weak, the whole claim becomes harder to defend.

For many businesses, this is where the claim either becomes clear and credible or vague and exposed. The role is not administrative. It goes to the centre of how qualifying R&D is assessed.

A competent professional is someone with the right qualifications or practical experience in the relevant field to judge whether a project sought an advance in science or technology and whether the answer was not readily deducible at the outset.

This is not just a question of seniority. A founder, CTO, technical director or lead engineer may be the right person, but title alone does not decide it. The real test is whether that person can explain:

That matters because HMRC does not assess a project against what was new to your business. It looks at what was known, or could readily be worked out, by a competent professional working in the field.

The competent professional matters because the core R&D test depends on expert technical judgement.

A claim needs someone who can explain why the project involved more than routine development, routine engineering, or ordinary problem-solving. That person should be able to show why the uncertainty was genuine, why the solution was not obvious at the outset, and why the work represented an advance in the field rather than only an internal improvement for the company.

This is also why weak claims often struggle. They may describe a complex commercial project, but they do not explain the underlying scientific or technological uncertainty clearly enough. Without a credible technical voice behind the narrative, the claim can drift into general business description rather than a defensible R&D position.

The competent professional can be internal or external, provided they have the right technical depth in the field that matters for the project.

In practice, that may be:

What matters is fit. If the project concerns embedded systems, complex software architecture, novel materials, process engineering, data infrastructure or medtech development, the competent professional should have genuine expertise in that area.

The wrong choice is often obvious in hindsight. A commercially senior person may know the business extremely well, but still be the wrong person to judge the underlying scientific or technological question.

The competent professional should help define four things clearly:

Question |

What the claim should show |

| What was the baseline? | What was already known or readily deducible in the field |

| What was the advance? | The improvement in science or technology being sought |

| What was the uncertainty? | Why the answer was not readily available at the start |

| Where did the R&D begin and end? | Which activities directly contributed to resolving that uncertainty |

This point is important because not every activity in a wider commercial project qualifies. A project may include concept design, trials, testing, scale-up, implementation, quality assurance, commercial deployment and customer support. Only some of those stages may involve qualifying R&D.

The competent professional helps identify the boundary properly. That creates a stronger technical narrative and usually supports better cost discipline too.

This is one of the most important distinctions in an R&D claim.

A technical challenge may be difficult, expensive, time-sensitive or commercially important. That does not automatically make it qualifying R&D.

A technological uncertainty exists where it is not readily deducible by a competent professional whether something is scientifically or technologically possible, or how it can be achieved in practice.

That is why businesses sometimes overstate qualifying activity. A project can involve real pressure, ambitious targets and demanding delivery work without meeting the R&D test. The issue is not how hard the work felt internally. The issue is whether the scientific or technological answer was genuinely uncertain at the outset.

No, but they should shape the technical case early and review it properly before submission.

Finance teams and advisers can structure the claim, prepare the cost analysis and assemble the filing. But the technical core should come from the person best placed to judge the advance and the uncertainty.

Where businesses often go wrong is timing. They draft a broad narrative first, then ask the technical lead to approve it at the end. That usually produces weak language, blurred boundaries and generic explanations.

A stronger process starts with the technical conversation. The competent professional should help define:

A name on a form is not enough. The claim should make clear why that person was the right person to judge the project.

Useful evidence may include:

That evidence does not need to dominate the page, but it should support the credibility of the technical narrative. A strong claim shows both the substance of the uncertainty and the credibility of the person explaining it.

Yes, but that does not remove the need for internal accountability. HMRC says the competent professional may be external. In some cases that is the best option, especially where the company lacks depth in-house.

At the same time, HMRC’s claims process still places responsibility on the claimant company. Where a claim notification is required, HMRC asks for the main senior internal R&D contact responsible for the claim. For the Additional Information Form, HMRC also expects project descriptions that explain the uncertainties and the activities used to resolve them, and it allows a separate report with more detail on methodology and competent professionals.

The practical answer is usually a blend. Internal technical owners provide project reality. Specialist advisers help turn that into a cleaner, more defensible claim.

The most common errors are usually straightforward.

Some companies default to the most senior person in the business. Others default to whoever signs off the claim. Neither approach is reliable. The competent professional should be chosen because of field-specific technical depth.

A weak claim often compares the project against what the company knew internally, rather than what was already known in the field. That makes ordinary development work sound more novel than it really was.

A project may be complex, expensive or commercially risky without involving qualifying R&D. The claim needs to show genuine scientific or technological uncertainty, not just a demanding delivery environment.

If the technical lead only sees the draft at the end, important detail is often missed. Baseline, uncertainty and project boundaries should be set early.

Phrases such as “complex project”, “significant challenge” or “innovative solution” do not carry enough weight on their own. The claim should say what was uncertain, why it was uncertain, and what work addressed it.

In software claims, the competent professional is often a senior architect, engineering lead or principal developer. The claim should explain why the uncertainty related to architecture, integration, performance, scalability, security or system behaviour, rather than standard development work.

In engineering claims, the competent professional may be a lead design engineer, process engineer or technical director. The narrative should show what was already known in the field, what constraints applied, and why the answer could not readily be worked out at the start.

In life sciences, the competent professional is often a senior scientist, formulation lead, technical director or specialist consultant. The claim needs to distinguish genuine scientific or technological uncertainty from regulatory, commercial or operational hurdles.

For leadership teams, the competent professional question is really about claim quality, governance and resilience.

If the technical ownership is weak, three problems usually follow:

That is why this issue matters beyond tax compliance. It affects cash flow, internal effort and confidence in the wider R&D claim process.

While the phrase competent professional is specific to UK R&D tax language, the underlying issue is broader. International groups still need the right technical decision-makers, consistent evidence standards and a clear link between technical work and claim preparation.

For businesses operating across multiple jurisdictions, that means balancing local technical depth with wider group-level governance. FI Group by EPSA supports clients through a model that combines global reach with local expertise, helping businesses align technical evidence with country-specific requirements while maintaining a clearer overall funding and innovation strategy.

FI Group by EPSA helps businesses identify the right competent professional, frame the baseline correctly, and build stronger technical narratives around qualifying R&D.

That can include:

If your business is carrying out genuine R&D but your claim still relies on broad project summaries, FI Group by EPSA can help turn technical complexity into a clearer, more defensible filing.

No. The role depends on technical competence in the relevant field, not board status.

Yes, if the CTO has the right technical depth in the field and can judge the baseline, the advance and the scientific or technological uncertainty.

Yes. An external expert may be appropriate where the company does not have enough in-house technical depth.

No. Different projects may require different specialists depending on the field and the uncertainty involved.

Not necessarily, but their judgement should shape the technical case and the way qualifying projects are described.

Useful records may include design notes, test results, technical meeting notes, failed attempts, prototype evidence and documents showing how the uncertainty was addressed.

Yes. Software projects still need someone qualified to judge whether scientific or technological uncertainty existed.

That may still be a genuine technical challenge for the business, but it is less likely to meet the R&D tax definition.

Ideally at the start of claim preparation, while project scoping and technical interviews are still underway.

With compliance checks up and rules tighter, R&D tax relief works best when the claim is built during the year, not after it. In-year claiming brings forward cash, lowers enquiry risk, and cuts the admin burden.

In-year claiming means compiling your R&D tax relief claim as you go, not filing the company tax return before the year end. You still file retrospectively once accounts are finalised. The difference is operational. You capture technical evidence and costs quarterly or biannually while projects are fresh, so the final claim is largely prepared already.

Three changes define today’s environment.

Alongside this, checks remain elevated. Around one in five claims face challenge, with enquiries taking close to eight months on average and more than three quarters reduced during review.

Most companies leave a minimum nine-month gap between spend and benefit because they assemble the claim after year end, then wait for accounts sign-off and processing. In-year claiming compresses that lag. By adopting in-year processes, businesses can often shift R&D tax relief from a 9–11 month wait into a 3 month benefit, depending on how quickly accounts are finalised and HMRC processes the return. You control two levers:

In-year practices directly address the common reasons for challenge, including poor technical evidence, malapportionment of software or consumables, and mis-treated EPWs or subcontractors. Enquiries now average more than 240 days and over three quarters of claims are reduced during checks, so building contemporaneous evidence is a practical risk reducer.

What is the effective benefit under the merged scheme?

The credit is 20% taxable and shown above the line. After 25% corporation tax the effective net benefit is roughly 15%.

Do overseas subcontractor costs still qualify?

From April 2024 most overseas costs are excluded, except in narrow circumstances such as unavoidable geography. Plan early.

What is ERIS and who qualifies?

ERIS supports loss-making SMEs that meet an R&D intensity threshold, which reduces to 30% from April 2024.

How long do enquiries take and how often are claims reduced?

Recent figures indicate enquiries average more than 240 days and over three quarters of claims are reduced during checks.

How does in-year claiming reduce risk?

It creates contemporaneous evidence, reconciled costs and an enquiry pack before filing, which shortens responses and raises confidence under scrutiny.

Merck has scrapped a planned £1bn UK expansion, will shift life sciences research to the US, and is cutting 125 UK roles, including an exit from London lab space near King’s Cross. For finance leaders, the signal is clear. UK projects face tighter ROI hurdles, so funding strategy, enquiry readiness, and cross-border optionality matter more than ever.

Merck will not proceed with the proposed £1bn UK expansion, will move a portion of life sciences research to the United States, and will close its London lab footprint with around 125 job losses. The company cited inadequate UK state investment and the undervaluation of innovative medicines, alongside more attractive conditions elsewhere.

Board debates on where to place R&D and scale-up work are becoming more pointed. The UK still has world-class science, but pricing pressures, adoption risk, and competition from the US and other regions heighten the bar for investment cases.

The decision reflects state investment gaps, pricing and adoption pressures, and stronger incentive ecosystems elsewhere. When future revenue visibility weakens, capital migrates to locations where reimbursement, uptake, and support combine to improve risk-adjusted returns.

Signals for UK-based portfolios:

“It is a great shame to see so much investment being pulled out of the UK life sciences market. A big reason behind this is that many smaller life sciences companies and research consortiums rely heavily on larger companies to facilitate partnerships and attract additional investment. This news only compounds that fact, and it may just be the start. In times like these, the finance edge comes from stacking non-dilutive funding and building audit-ready claims that travel well across jurisdictions.” – Dr. Giuseppe Amoroso, Senior R&D Tax Consultant, FI Group UK.

Expect tougher internal hurdle rates and more scrutiny of UK siting decisions. To preserve UK optionality, pair stacked non-dilutive funding with audit-ready claims and a cross-border incentive plan that the Board trusts.

Three finance realities now in play:

Stack funding, build an enquiry-ready evidence pack, and prepare cross-border options. Combine UK R&D tax relief with targeted grants, map every cost to the correct regime, and appoint one accountable partner to coordinate incentives across jurisdictions.

The UK remains competitive when R&D tax relief is paired with mission-fit grants and strong enquiry defence. CFOs should combine mechanisms and calibrate by project stage.

If your Board demands optionality, FI Group bridges strategy at HQ to execution in-country. We coordinate UK claims with US federal and state credits, European programmes, and LATAM/APAC incentives through one accountable lead.

What this looks like in practice:

Global Reach. Local Expertise. Your HQ sees the full picture. Your teams feel the local support.

| Objective | Primary lever | What good looks like | How FI Group de-risks it |

| Stabilise UK project ROI | R&D Tax Relief | Clear uncertainty narrative, systematic approach, reconciled costs | Technical interviews, dossier build, CT600 and AIF mapping, enquiry defence playbook |

| Accelerate milestones | Innovate UK or EU collaboration grants | Funding aligned to clinical and manufacturing milestones | Bid strategy, consortium formation, cost allocation and subsidy control checks |

| Maintain optionality | US, LATAM, APAC incentives | Pre-approved routes, timeline and cost comparisons | Single governance model with local experts and unified Board reporting |

| Reduce enquiry risk | Pre-submission QA | Independent review of narratives and calculations | Standard checklists, sampling, audit trail, version control |

| Improve forecastability | Master incentives calendar | One view of deadlines and rules by country | Central PMO, country playbooks, quarterly refresh cadence |

Is the UK now uninvestable for pharma?

No. The UK still offers outstanding science and talent. However, pricing, adoption and investment intensity vary. Your task is to stack incentives, shore up evidence, and keep cross-border options open so Board decisions do not stall.

Can we combine grants and R&D tax relief?

Often yes, with careful structuring. You must prevent double counting and respect subsidy rules. Map every cost by project and funding source, and align calculations to the correct regime for your accounting period.

What makes an R&D claim enquiry-ready in life sciences?

A tight technical narrative tied to technological uncertainty, an indexed evidence pack, named staff time linked to payroll, supplier evidence, and a clean reconciliation to your CT600 and Additional Information Form.

How does a one-team global model actually help Finance?

It reduces internal burden, centralises risk management, and ensures consistent quality across regions. That shortens cycles and improves audit outcomes while giving the Board a clear line of sight.

FI Group is a strategic advisory partner to CFOs, Heads of Tax, and Group Executives. We combine global reach with local expertise, delivering one governance framework across jurisdictions, with specialist authors and tax professionals in-country. Results include lower internal effort, higher claim quality, stronger audit defence, and accelerated rollout of funding across your portfolio.

Call to action: Talk to us about a stacked, cross-border funding plan that protects your UK pipeline while unlocking international support.

CFOs and founders increasingly recognise that growth cannot be fuelled by equity alone. The most successful scale-ups blend venture capital with non-dilutive funding, such as R&D tax relief, innovation grants, and government-backed loans. This strategy reduces dilution, extends runway, and validates technology in ways that strengthen investor confidence and speed market entry.

This guide sets out a CFO playbook for combining funding sources across the UK and Europe, with FI Group’s global-local delivery model ensuring compliance and consistency at every step.

A balanced innovation funding strategy deliberately mixes private equity with non-dilutive instruments. These include:

The goal is to make each pound of equity raised work harder, while reducing burn rate and aligning milestones with investor expectations. A balanced approach also provides external validation, as competitive grants and compliant R&D claims send strong quality signals to boards, auditors, and shareholders.

Every pound of grant or tax credit is a pound you do not need to raise in equity. This means more milestones can be reached without handing over additional equity, helping founders and early investors keep control.